My first job at 13 was at The Popcorn Stand. I made $5.50 an hour and cherished every hundred dollar paycheck. I was the Popcorn Godfather!

Times have changed over the years but I’ve always loved the making and collecting of money. The spending part has never been my interest. In general, I love this man-made invention of green paper and how it impacts our society.

“Money is not everything but it enables everything.”

There are infinite articles about how to make money but a complete absence about what you do once you get it. It’s something I constantly ask wealthier friends what they do so I can improve my own.

I am going to share what I do with my money in hopes that we all can share and learn with each other.

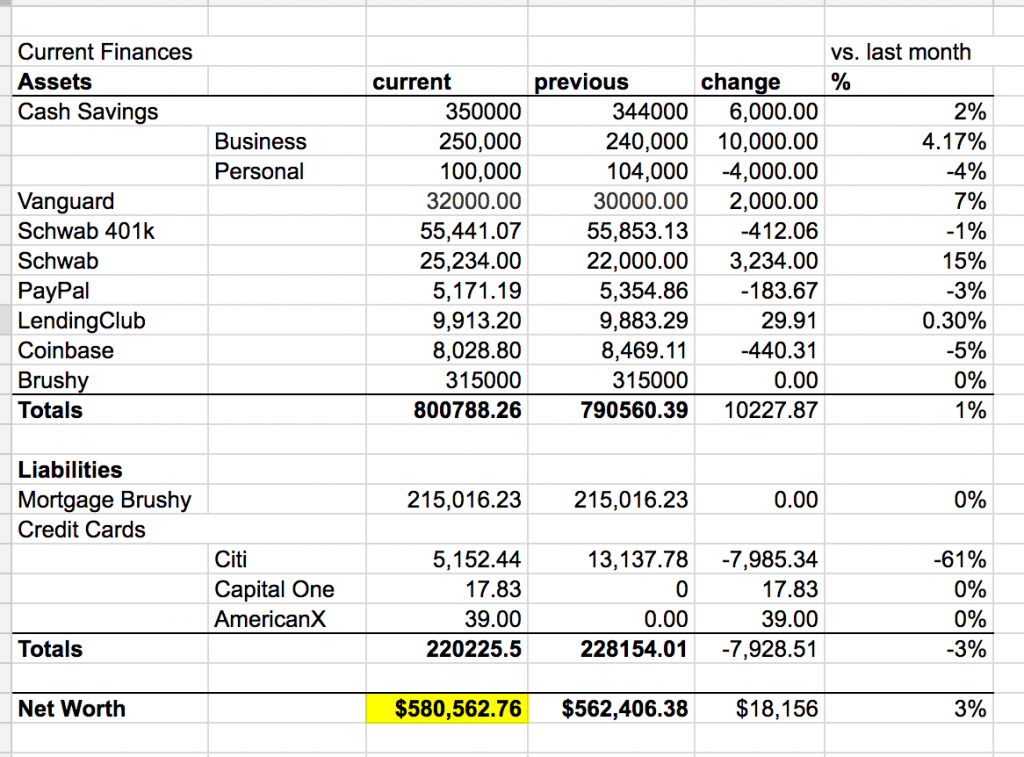

Everything for me starts with my monthly Google Spreadsheet.

| BONUS: Click here to get my Spreadsheet |

Every month I make a copy of the spreadsheet and manually update it. I like the intention that I have to do check all the different sites and it makes me feel confident I’m seeing the real numbers.

There are automation options I recommend like Mint and Personal Capital. A lot of guys in our Sumo office really like Digit for automated savings or Robinhood for buying stocks.

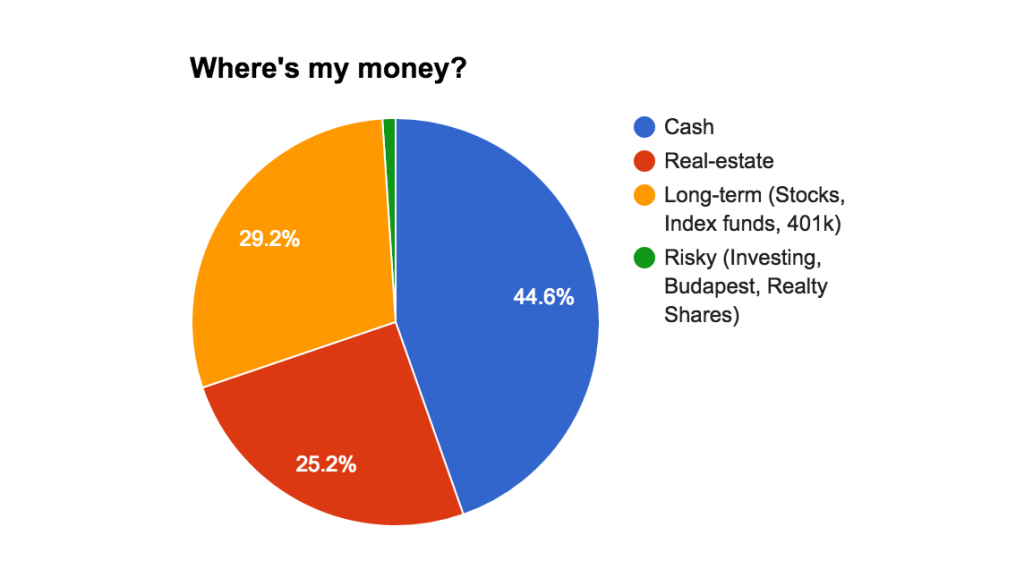

Here’s how I breakout my money:

45% – Cash

25% – Real estate

25% – Long-term (stocks)

5% – Risky

Cash

Most of my money is in cash since I like KNOWING where my money is at ALL times. When the economy goes bad, the people with cash in hand will be in charge. Yes, I know inflation blah blah, whatever the F that is. But, it gives me flexibility for opportunities to make large cash purchases vs requiring a loan from anyone.

Long-term (stocks)

Let me just say it. I am the worst stock investor ever. You should create a fund that just shorts everything I buy. Here’s a list of some of my “best” stock buys:

- KKR – I liked the company from Barbarians at the Gate book, lost $4,000

- Shake Shack – Hardly ate there but supposedly they are always crowded, lost $3,000

- Chipotle – Hello ebola, lost $1,700 (so far)

- BlockBuster – Don’t ask

Clearly, you can see I’m the greatest stock picker ever.

So I buy a few stocks that I just love like Amazon, Google, Tesla and 2 with great dividends: AT&T and Verizon. I don’t plan on selling these stocks and hold them for the very long term.

What Warren Buffet famously suggested and I do is move the majority of my market investing to index funds. Why? It’s been consistently shown that index funds outperform many individual stock pickers + hedge funds.

This money is specifically in Vanguard Small Cap and Vanguard Wellington Large Cap.

Every month $1,000 from my paycheck is automatically withdrawn to buy shares of the above index funds.

I don’t think I’ll live to 65, so I prefer to put my money directly in the above investments instead of a 401k or IRA. If you are a small business owner yourself, check out the SEP IRA if you think you’ll live longer than me 🙂

Real-Estate

How many people can buy real estate? Almost EVERYONE.

How many people think they are great at real estate? Way too many people (and most of them aren’t).

How many people are pretty darn good at online business? Very few.

Thankfully I’m one of them. Lesson: Play to your strengths. I’ve come to recognize real estate is good but as a profit center it’s not the best use of my time.

I have 4 properties. There, I said it. “Wow, he must be so rich” you’re thinking. But in reality the amount of money I make a YEAR in real-estate is way less than what we make in ¼ a month at AppSumo.

Don’t get me wrong, it’s a better return than just leaving it in my checking account. But that comes at the cost of dealing with A/C issues, tenants being meanie weenies and other distractions.

In addition, I use RealtyShares.com, which is a way of giving money to professional real-estate investors. I’ve put in around $60k so far and make around 10% cash on cash return from that. Not a guaranteed return but a way of diversifying my real-estate amounts without the hassle of the day-to-day involvements.

Risky

This is money I don’t mind losing at all. It’s money to invest in myself and learn about new things. If it makes money, all the better.

Here’s what I’ve done with it:

Invested money in Teachable.com and Buffer.com. Both are companies I highly recommend. I get insight into how they run their company, financials and more. It’s like an advanced Ph.D. class that is WAY cheaper than paying for college.

Another risky investment was giving a friend $40k for him to try out AirBnB in Los Angeles. I was curious how the business model of renting out places worked. I made that money back and now get 15% profit from one of the places, thanks Zack!

I gave a friend $1,000 who’s making a fitness product called the Fit Fly shaker. If the money doesn’t come back, that’s fine. I’m happy to support and learn more about physical products.

Lastly, an acquaintance was buying a church in San Antonio and I wanted to learn the economics of commercial real estate so I decided to invest in him. Made back around 5% so it’s not been a great return, but seeing first hand how a pro real estate person works has been worth it.

——

Hope this helps you learn something for you to improve your own personal finances.

Leave a reply and let me know what you do with YOUR finances.

16 responses to “Where’s my money?”

“Great! Can you please update the link to the template? It’s not working right now 🙂

Hi Noah

No crypto currency ?

I’m the Editor at EarlyToRise.com and I’d love to republish this article for our readers, linking back to this original post. Would that be alright?

You are doing everything wrong except having a lot of cash around. No wonder all these newly quick rich kids are losing everything. You need help and don’t even know it…when the eventual hiccup comes, you will feel it but because you have a lot of cash, you will survive…maybe. I’d have to know more cash flow info to see if you’d be back on the streets pounding the next idea or not. Sorry man…

Thanks for sharing your personal finance overview. Really helps to visualize how things should be done to be eventually be financially secure and independent.

I disagree with so much money invested in cash. Investing it in long-term stocks is a better idea.

I like the idea that you invest in Start Up Ideas, I would read Rich Dad books and use them and apply it to tech related businesses as you are doing.

useful, for life and living ?thanks

I hold a lot of cash too, not nearly as much as a percentage of total net worth, and I like the security and flexibility of cash. I’m willing to “pay,” in lost returns, to have flexibility because it gives you options. All too often people want to be super efficient and get the maximum return on everything, but we forget that it comes with a non-financial cost like stress and opportunity cost.

Love it – I call it where do we stand – what I do. You need to take educated risks to get rewards. Thanks for sharing.

I’m also doing a monthly update on a spreadsheet since about 3 years now. My net worth is slowly growing and i got a much better grasp on my financial situation.

I absolutely love Digit, it makes saving so easy. For investments, beyond my standard ‘traditional’ stuff I also am really liking Acorns. It takes change from your purchases and uses them to buy stocks based on risk levels.

Thanks for sharing Noah, your “risky” section contains some fascinating alternative investment ideas.

Do you find mixing your business cash holdings in with your personal holdings creates a distorted picture? The bank and the tax man may take a different point of view as to what is yours versus what belongs to your business.

The folks in Brazil probably thought “inflation blah blah” right up until their economy tanked recently and their inflation rate shot up to 9%! You’re too smart a bloke not to have your cash stashed someplace where it is earning a higher than inflation return. Care to share? Perhaps a reasonably liquid peer-to-peer lender like FundingCircle for example?

I like the idea of a monthly spreadsheet. Looks like a great way to keep an eye on what goes where.

Not contributing to a 401(k)? Ugh Noah. You’re doing it wrong. It’s the right move even if you die at 65. I’ll have to write up a post on this.

-Josh

I like using the barbell strategy (learnt from Nassim Nicholas Taleb) – where most of the weight (risk) is at the edges. 80-85% very conservative investments (index funds, fixed deposits, 1 commercial rental property). 15-20% high risk investments (bitcoin, startups. selected small cap equity stocks). One of the plus points of being from India is that Indian banks give 8% returns on savings, and Indian stock market is showing double digit growth – and so even the conservative investments have done well. Not sure how long that will last however.